{kind=link}

[ad_1]

Final 12 months, our report on cloud adoption confirmed that firms had been shifting shortly to undertake the cloud: 88% of our respondents from January 2020 stated that they used the cloud, and about 25% stated that their firms deliberate to maneuver all of their functions to the cloud within the coming 12 months.

This 12 months, we wished to see whether or not that development continued, so we ran one other on-line survey from July 26, 2021, to August 4, 2021. For the reason that 2020 survey was taken when the pandemic was looming however hadn’t but taken maintain, we had been additionally inquisitive about how the lockdown affected cloud adoption. The brief reply is “not a lot”; we noticed surprisingly few modifications between January 2020 and July 2021. Cloud adoption was continuing quickly; that’s nonetheless the case.

Study quicker. Dig deeper. See farther.

Government abstract

- Roughly 90% of the respondents indicated that their organizations are utilizing the cloud. That’s a small improve over final 12 months’s 88%.

- The response to the survey was international; all continents (save Antarctica) had been represented. In comparison with final 12 months, there was a a lot increased proportion of respondents from Europe (33%, versus 11%) and a decrease proportion from North America (42%).

- In each trade, not less than 75% of the respondents work for organizations utilizing the cloud. Essentially the most proactive industries are retail & ecommerce, finance & banking, and software program.

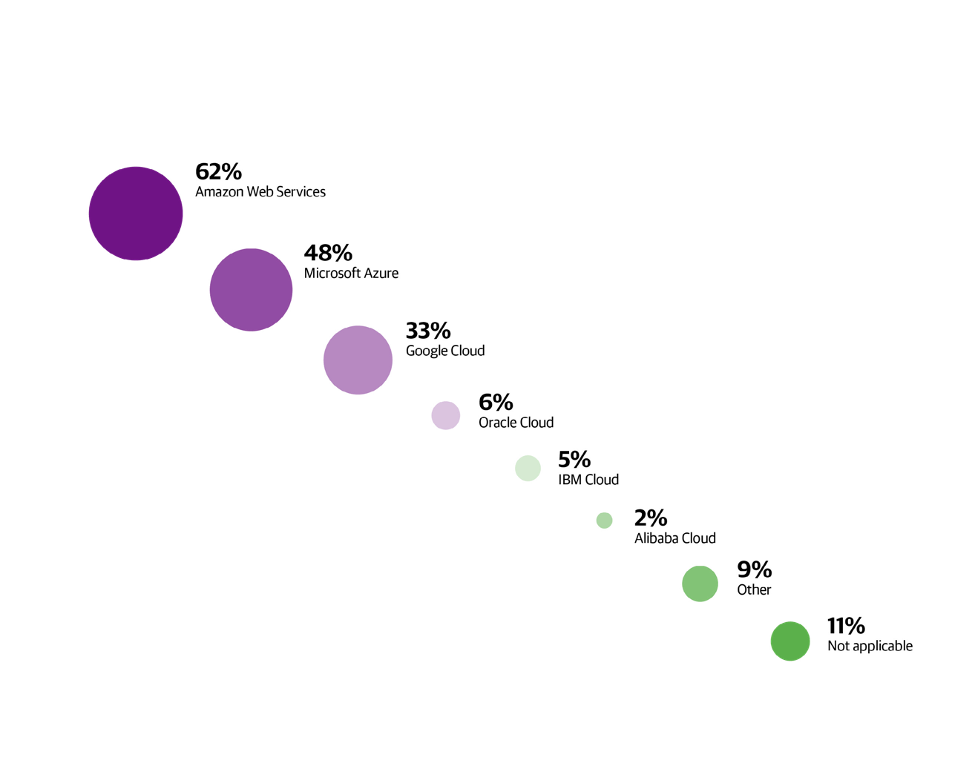

- Amazon Internet Companies (AWS) (62%), Microsoft Azure (48%), and Google Cloud (33%) are nonetheless the massive three, although Amazon’s market share has dropped barely since final 12 months (down from 67%). Most respondents use a number of cloud suppliers.

- Business to trade, we noticed few variations in cloud suppliers, with two exceptions: Azure is used extra closely than AWS within the authorities and consulting & skilled companies sectors.

- Two-thirds of respondents (67%) reported utilizing a public cloud; 45% are utilizing a non-public cloud; and 55% are utilizing historically managed on-premises infrastructure.

- Virtually half (48%) stated they plan emigrate 50% or extra of their functions to the cloud within the coming 12 months. 20% plan ti migrate all of their functions.

- 47% stated that their organizations are pursuing a cloud first technique. 30% stated that their organizations are already cloud native, and 37% stated that they plan to be cloud native inside three or extra years. Solely 5% are engaged in “repatriation” (bringing cloud functions again to on-premises infrastructure).

- Amongst respondents who’re utilizing the cloud, the most important concern is managing price (30%). Compliance is a comparatively minor concern (10%) and isn’t essentially the most important concern even in closely regulated sectors corresponding to finance & banking (15%), authorities (19%), and healthcare (19%).

- When requested what expertise organizations wanted to succeed, respondents had been divided pretty evenly, with “cloud-based safety” (59%) and “common cloud information” (54%) the commonest responses.

Demographics: Who responded

The survey was despatched to recipients of O’Reilly’s Programming and Infrastructure & Ops Newsletters, which collectively have 436,000 subscribers. 2,834 respondents accomplished the survey.

The respondents characterize a comparatively senior group. 36% have over 10 years’ expertise of their present position, and virtually half (49%) have over seven years’ expertise. Newer builders had been additionally well-represented. 23% have spent one to 3 years of their present place, and eight% have spent below one 12 months.

Parsing job titles is all the time problematic, on condition that the identical place might be expressed in many various methods. Nonetheless, the highest 5 job titles had been developer (4.9%1), software program engineer (3.9%), CTO (3.0%), software program developer (3.0%), and architect (2.3%). We had been shocked by the variety of respondents who had the title CTO or CEO. No one listed CDO or chief information officer as a title.

Aggregating phrases like “software program,” “developer,” “programmer,” and others lets us estimate that 36% of the respondents are programmers. 21% are architects or technical leads. 10% are C-suite executives or administrators. 8% are managers. Solely 7% are information professionals (analysts, information scientists, or statisticians), and solely 6% are operations employees (DevOps practitioners, sysadmins, or website reliability engineers).

The respondents got here from 128 completely different nations and had been unfold throughout all continents apart from Antarctica. Many of the respondents had been from North America (42%) and Europe (33%). 13% had been from Asia, although that nearly definitely doesn’t mirror the extent of cloud computing in Asia.

Specifically, there have been few respondents from China: solely 8, or about 0.3% of the full. South America, Oceania, and Africa had been additionally represented, by 6%, 4%, and a pair of% of the respondents, respectively. These outcomes are considerably completely different from final 12 months’s. In 2020, two-thirds of the respondents had been from North America, and solely 11% had been from Europe. The opposite continents confirmed little change. Final 12 months, we famous that European organizations had been reluctant to undertake the cloud. That’s clearly not true.

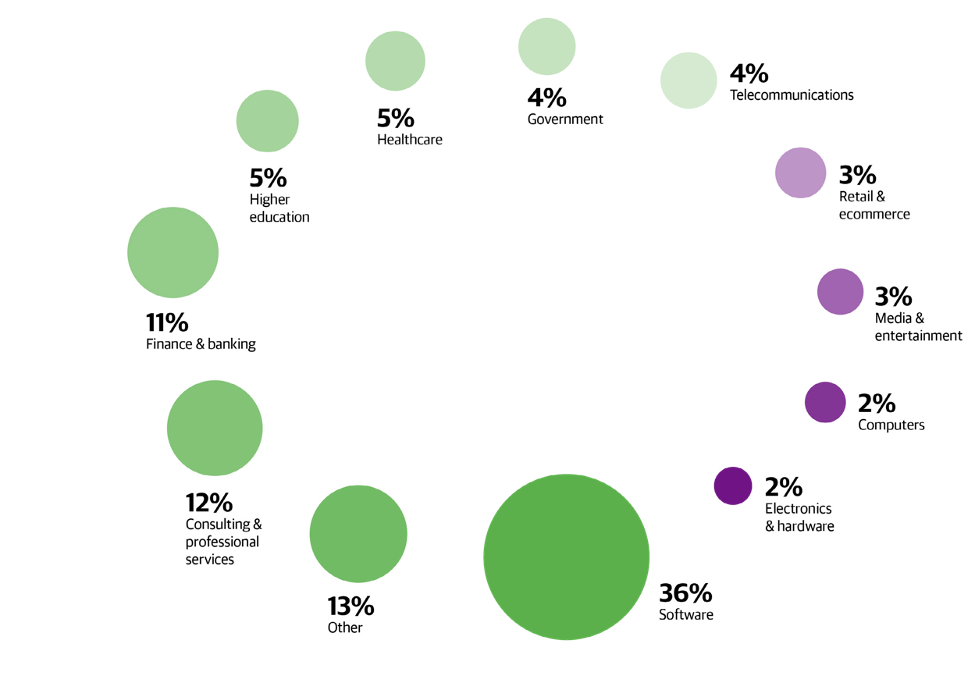

Cloud customers are unfold all through the economic spectrum. Respondents to our survey had been clustered most strongly within the software program trade (36%). The following largest group contains these who replied “different” (13%), and they’re certainly scattered by way of industries from artwork to aviation (together with some outliers like prophecy, which we by no means knew was an trade). Consulting & skilled companies (12%) was third; we suspect that many respondents on this group may equally properly say they had been in the software program trade. Finance & banking (11%) was additionally well- represented. 5% of the respondents work in healthcare; one other 5% had been from increased schooling; 4% had been in authorities; and a complete of 4% work in electronics & {hardware} or computer systems (2% every). Surprisingly, solely 3% of the respondents work in retail & ecommerce; we’d have anticipated Amazon alone to account for that.

These outcomes are similar to the outcomes from final 12 months’s survey, with two main variations: this 12 months, an excellent bigger proportion of our respondents had been from the software program trade (23% in 2020), and a considerably bigger group categorized their industries as “different” (20%).

What does this imply? Lower than it appears. We have now to remind each ourselves and our readers that the variety of respondents in any sector displays, first, the scale of that sector; second, our mailing lists’ penetration into that sector; and solely third, cloud utilization in that sector. The truth that 35% of the respondents are within the software program trade whereas solely 5% are in healthcare doesn’t by itself imply that the cloud has penetrated far more deeply into software program. It signifies that the healthcare trade has fewer readers of our newsletters than does the software program trade, hardly a stunning conclusion. To estimate cloud utilization in any given sector, it’s a must to look solely at that sector’s information. What it says is that our conclusions concerning the software program trade are primarily based on roughly 1,000 respondents, whereas conclusions concerning the healthcare trade are solely primarily based on about 150 respondents, and are correspondingly much less dependable.

The massive image

The massive image gained’t shock anybody. Virtually all the respondents work for organizations which are utilizing cloud computing; solely 10.3% answered a query asking why their group doesn’t use cloud computing, implying that cloud utilization is 89.7%. Likewise, when requested what cloud supplier they’re utilizing, 10.7% stated “not relevant,” suggesting cloud utilization of 89.3%. We will get a 3rd repair on cloud utilization by taking a look at a later query about cloud applied sciences. We requested whether or not respondents are utilizing public clouds, personal clouds, hybrid clouds, multiclouds, or historically managed

infrastructure. Respondents had been allowed to pick a number of solutions, and most did. Nonetheless, respondents whose organizations aren’t utilizing any cloud expertise would examine “historically managed infrastructure.” These respondents amounted to 7.5% of the full, suggesting 92.5% of the respondents are utilizing the cloud in some kind. Due to this fact, we will say with some confidence that the variety of respondents whose organizations are utilizing the cloud is someplace between 89% and 93%.

These figures evaluate with 88% from our 2020 survey—a change that might be insignificant. Nonetheless, it’s value asking what “insignificant” means: would we count on the variety of “not utilizing” responses to be close to zero? On one hand, we’re shocked that there hasn’t been a bigger change from 12 months to 12 months; alternatively, whenever you’re already close to 90%, gaining even a single proportion level is troublesome. We might be considerably (solely considerably) assured that there’s a real development as a result of we requested the identical query three other ways and acquired comparable outcomes. A further proportion level or two could also be all we get, even when it doesn’t permit us to be as assured as we’d like.

Did the pandemic have an impact? It definitely didn’t gradual cloud adoption. Cloud computing was an apparent answer when it grew to become troublesome or inconceivable to employees on-premises infrastructure. You possibly can argue that the pandemic wasn’t a lot of an accelerant both, and it could be arduous to disagree. As soon as once more although, whenever you’re at 88%, gaining a proportion level (or two or three) is an achievement.

AWS, Azure, and Google Cloud: The massive three and past

The massive three in cloud computing are Amazon Internet Companies (AWS), Microsoft Azure, and Google Cloud, utilized by 62%, 48%, and 33% of the respondents, respectively. (As a result of many organizations use a number of suppliers, respondents had been allowed to pick a couple of choice.) Oracle Cloud (6%), IBM Cloud (5%), and Alibaba Cloud (2%) took fourth by way of sixth place. They’ve a protracted technique to go to catch as much as the leaders,

though Oracle appears to have surpassed IBM. It’s additionally value noting that, though Alibaba’s 2% appears weak, we count on Alibaba to be strongest in China, the place we had only a few respondents. Higher visibility into Chinese language trade may change the image dramatically.

9% of the respondents chosen “different” as their cloud supplier. The main “different” supplier was Digital Ocean (1.4%), which just about edged out Alibaba. Salesforce, Rackspace, SAP, and VMware additionally appeared among the many “others,” together with the Asian supplier Tencent. Many of those “different” suppliers are software-as-a-service firms that don’t present the sort of infrastructure companies on which the massive three have constructed their companies. Lastly, 11% of the respondents answered “not relevant.” These are presumably respondents whose organizations aren’t utilizing the cloud.

In comparison with final 12 months, AWS seems to have misplaced some market share, going from 67% in 2020 to 62%. Microsoft Azure and Google Cloud stay unchanged.

Cloud utilization by trade

One purpose of our survey was to find out how cloud utilization varies from trade to trade. We felt that one of the simplest ways to reply that query was to go at it in reverse, by wanting on the respondents who answered the query “What finest describes why your group doesn’t use cloud computing?” (which we’ll talk about in additional element later). Our outcomes supplied different methods to reply this query—for instance, by taking a look at “not relevant” responses to questions on cloud suppliers. All approaches yielded considerably the identical solutions.

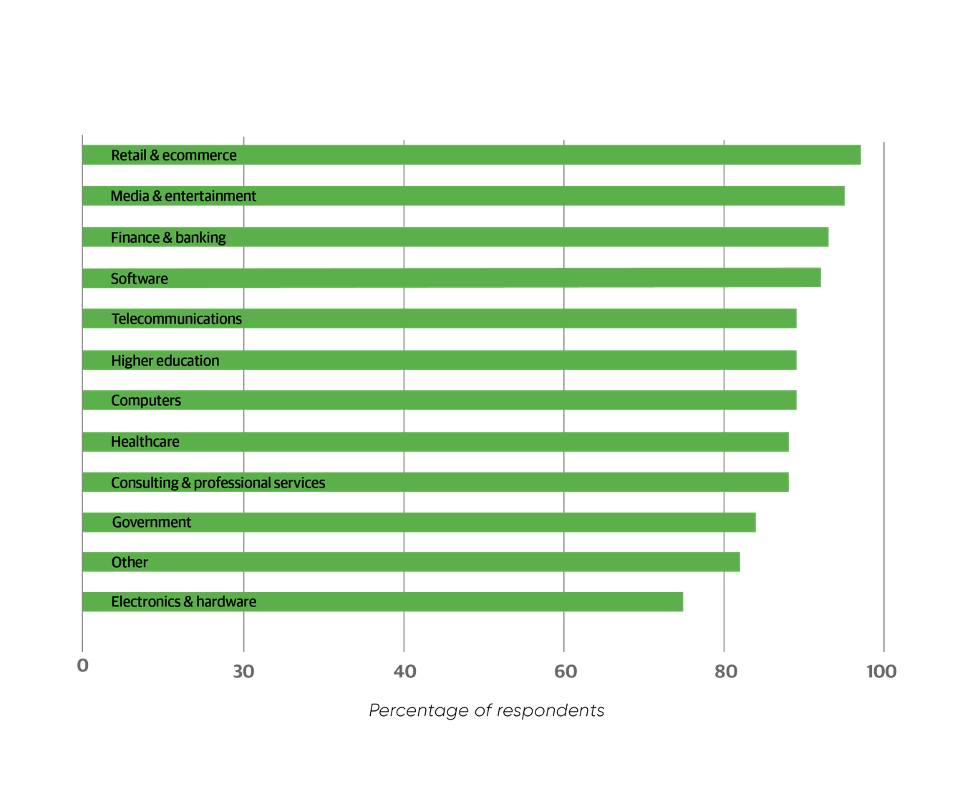

We discovered that retail & ecommerce, media & leisure, finance & banking, and software program stand out because the trade sectors with the very best cloud use. Solely 3.1% of the respondents from the retail & ecommerce sector answered this query, indicating that cloud utilization was near common (96.9%). 5.1% of the respondents in media & leisure, 7.2% of the respondents in finance & banking, and seven.5% of the respondents in software program answered this query, suggesting 94.9%, 92.8%, and 92.5% cloud utilization, respectively. Most industries (together with healthcare and better schooling) clustered round 10% of organizations that aren’t utilizing the cloud, or 90% cloud utilization. Essentially the most cloud-averse industries had been electronics & {hardware} (with 25% indicating that they don’t use the cloud) and authorities (16% not utilizing). However take into account: 25% of respondents indicating that they don’t use the cloud implies that 75% of the respondents do. Whereas we noticed variation from trade to trade, cloud customers are a stable majority all over the place.

Can we get past the numbers to the “why”? Maybe not with out a way more detailed survey, however we will make some guesses. Though we had few respondents from the retail & ecommerce sector, it’s necessary to notice that this trade is the place the cloud took off: AWS started when Amazon began promoting “extra capability” in its information facilities. Jeff Bezos paved the best way for this together with his well-known “API mandate” memo, which required all software program to be constructed as collections of companies. In media & leisure, Netflix has been very public about its cloud technique. The corporate depends on the cloud for all of its scalable computing and storage wants, an method initially undertaken as a means of avoiding on-premises infrastructure as a single level of failure.

However historical past usually counts for little in tech. What’s extra necessary is that retail & ecommerce is a sector topic to large fluctuations in load. Black Friday is approaching as we publish this; want we are saying extra? In case your ecommerce website slows to a crawl below heavy load, you lose gross sales. The cloud is a perfect answer to that downside. No CIO desires to construct an on-premises information heart that may deal with 100x modifications in load. The identical is true for Netflix, although maybe to not the identical diploma: a brand new film launch virtually definitely creates a spike in visitors, presumably an enormous one. And within the

previous few years, film studios, distributors like Amazon, and lots of others within the trade have realized that the way forward for films lies in promoting subscriptions to streaming companies, not cinema tickets. Cloud applied sciences are perfect for streaming companies.

Nearly each software program firm, from startups to established distributors like Microsoft and Adobe, now affords “software program as a service” (SaaS), an method arguably pioneered by Salesforce. Whether or not or not subscription companies are the way forward for software program, most software program firms are betting closely on cloud choices, they usually’re constructing these choices within the cloud.

Understanding why banks are shifting to the cloud could also be tougher, however we predict it comes all the way down to focusing in your core competence. The finance & banking trade has traditionally been very conservative, with organizations going for many years with out important change to their enterprise fashions or procedures. Prior to now decade, that stability has gone out the window. Monetary service firms and banks are actually providing on-line and cellular merchandise, funding companies, monetary planning, and far more. One of the simplest ways to service these new functions isn’t by constructing out legacy infrastructure designed to help legacy functions largely unchanged because the starting of computing; it’s by shifting to an infrastructure that may scale on demand and that may be shortly tailored to help new functions.

Our subsequent step was to have a look at the cloud suppliers to find out what suppliers are utilized by every trade. Are some suppliers used extra broadly in sure industries than in others? Once we checked out this query, we noticed a well-known sample: AWS is essentially the most broadly used, adopted by Microsoft Azure and Google Cloud. AWS dominates media & leisure (79%) and is essentially the most generally used supplier in each sector apart from consulting & skilled companies (58%, in comparison with Azure at 60%) and authorities (52%, in comparison with Azure at 59%).

Along with authorities and consulting & skilled companies, Azure is broadly utilized in finance & banking (55%). That shouldn’t be stunning given the historic prominence of Microsoft Workplace on this trade.

Google Cloud was third in each sector apart from media & leisure (35%), the place it edged out Azure. It’s strongest within the consulting & skilled companies sector (41%) and the comparatively small computer systems sector (40%) and weakest in authorities (16%), healthcare (25%), and finance & banking (29%).

Electronics & {hardware} had the best variety of respondents who answered “not relevant” (28%). Though there have been surprisingly few respondents from the retail & ecommerce sector, it had the fewest (3%) respondents who answered “not relevant.”

AWS’s, Microsoft Azure’s, and Google Cloud’s shares had been closest to one another within the increased schooling sector (49%, 43%, and 39%, respectively).

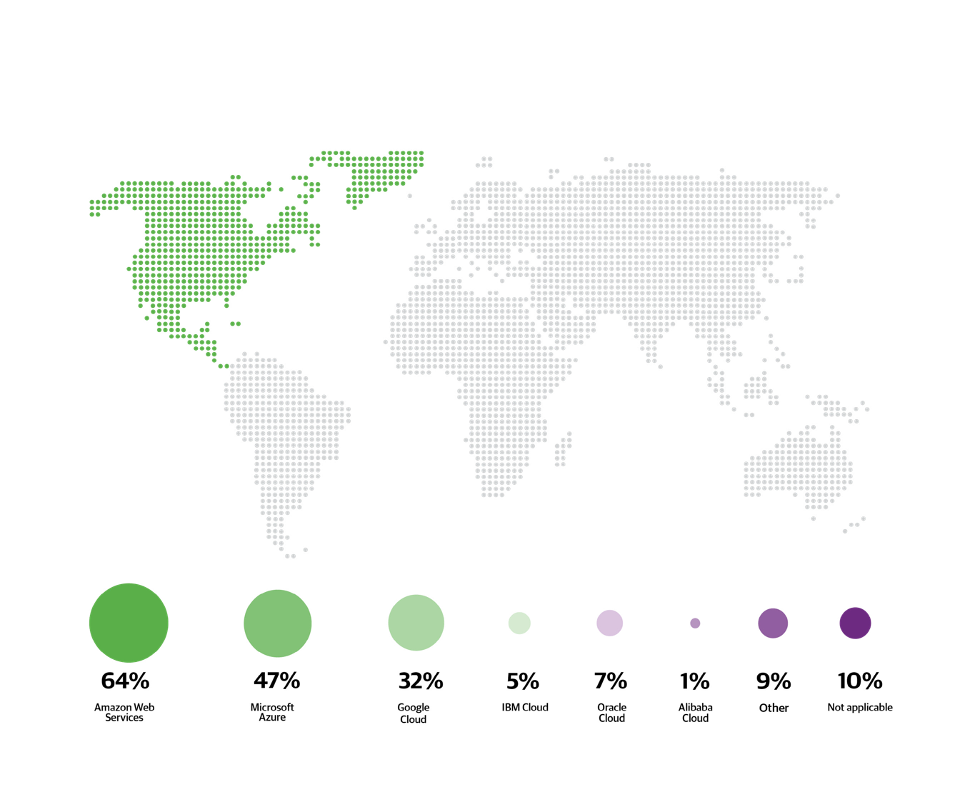

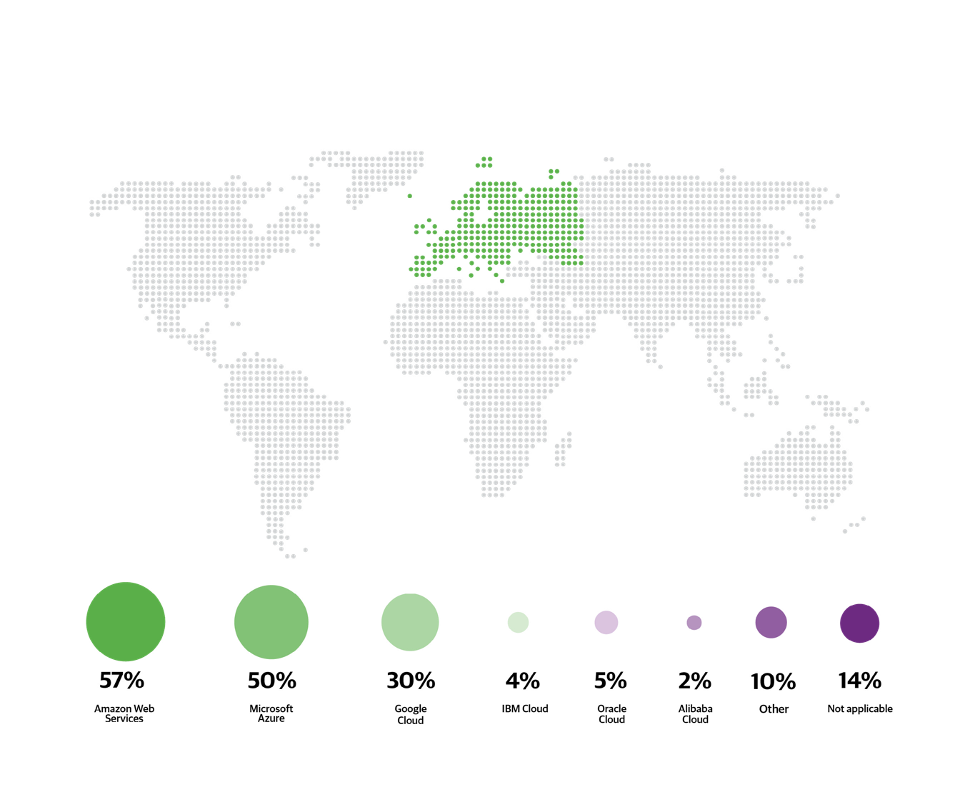

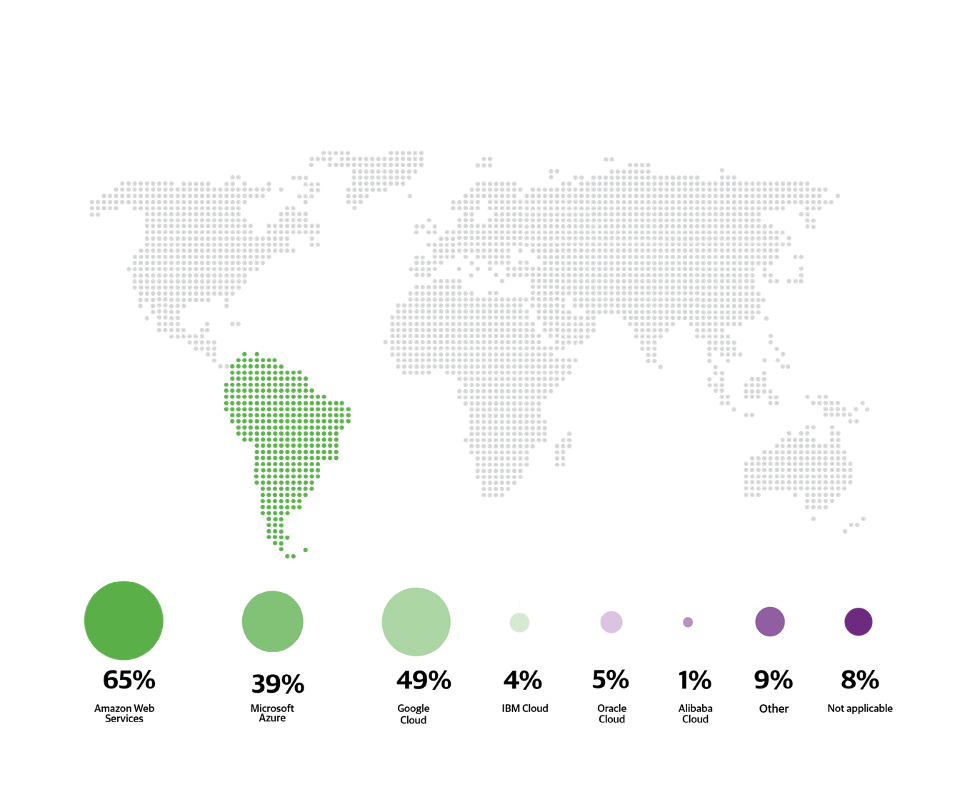

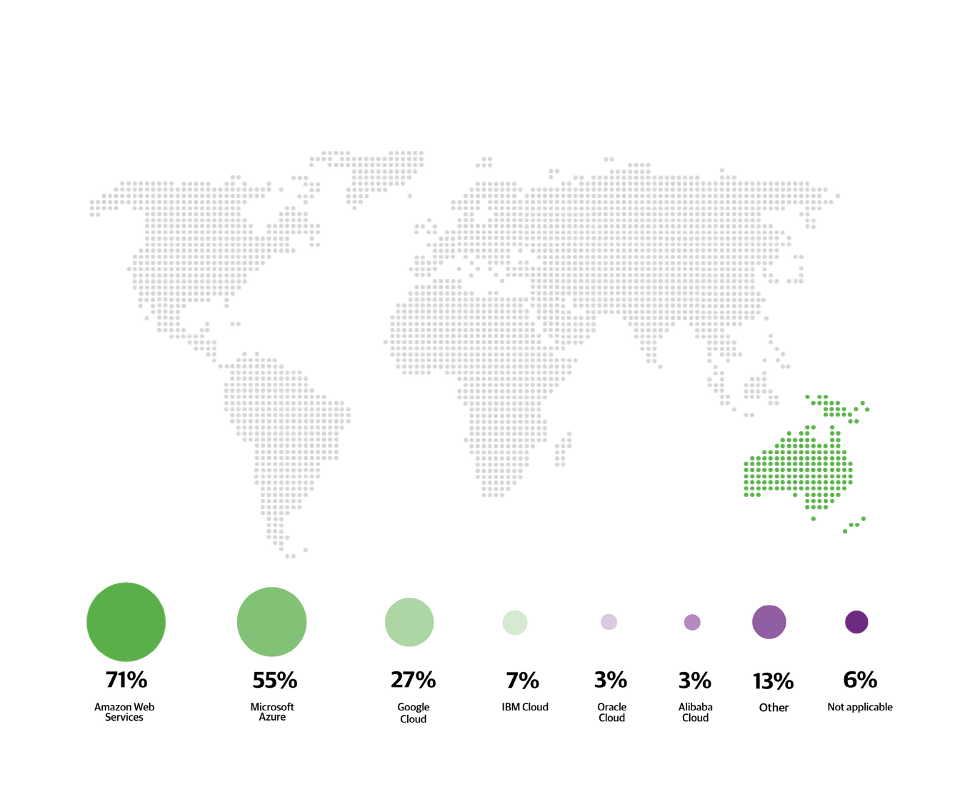

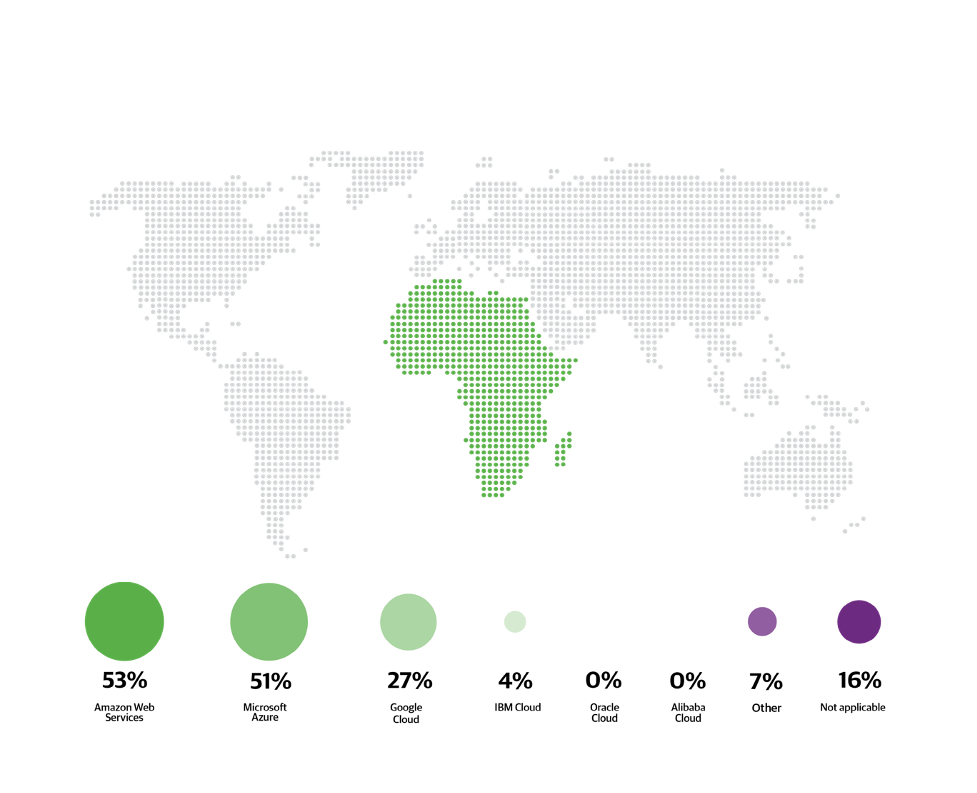

Cloud utilization by geography

We puzzled whether or not the utilization of various cloud suppliers diversified by continent: are some cloud suppliers extra widespread on some continents than on others? By and enormous, the reply isn’t any. AWS leads by a considerable margin on each continent, and Microsoft Azure and Google Cloud take second and third place, although their relative strengths fluctuate. Google Cloud is considerably stronger in South America (49%) and Asia (40%) than on the opposite continents. Azure is strongest in Oceania (55%), Africa (51%), and Europe (50%).

Alibaba Cloud is a considerably extra frequent selection in Asia (5%) and Oceania (3%), however not sufficient to vary the image considerably. Bear in mind, although, that we had few respondents from China, the place we suspect that cloud adoption is critical and Alibaba is a robust contender.

Though the odds are comparatively small, it’s additionally value noting that extra respondents in Oceania are utilizing “different” suppliers (13%), presumably as a result of their relative geographic isolation makes native cloud suppliers extra engaging, and that a big proportion of respondents in Europe answered “not relevant” (14%), indicating that cloud adoption should still be lagging considerably.

North America

Europe

Asia

South America

Oceania

Africa

Whereas we’ll talk about multicloud in additional element later, it’s attention-grabbing that this diagram provides some hints concerning the extent of deployment on a number of clouds. Do not forget that respondents may and incessantly did choose a number of cloud suppliers, so the full proportion in any continent (all the time higher than 100%) is a really tough indicator of a number of cloud deployments. By that measure, Africa (totaling 142%) and Europe (158%) have the fewest a number of cloud deployments; Oceania (179%) has essentially the most.

Public or not

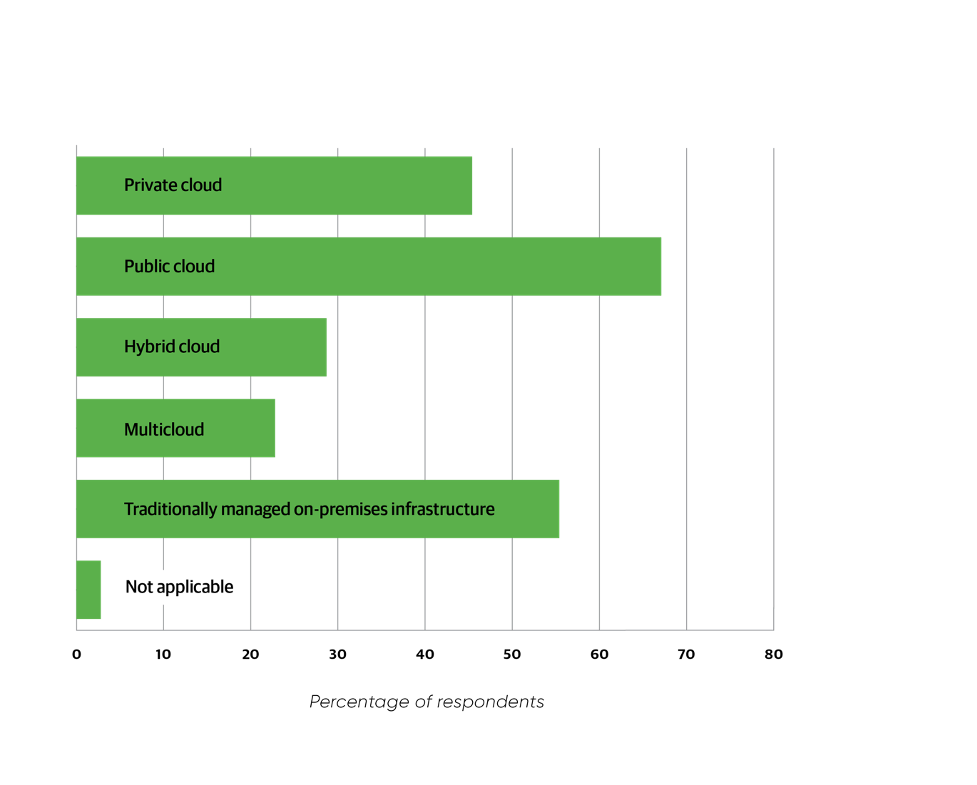

We requested our respondents what cloud applied sciences they’re utilizing. 67% (two-thirds) are utilizing a public cloud supplier, corresponding to AWS, versus 61% in 2020. 45% are utilizing a non-public cloud—personal infrastructure (on-premises or maybe hosted) that’s accessed utilizing cloud APIs—which represents a ten% improve over 2020 (35%). And 55% are utilizing historically managed on-premises infrastructure, versus 49% final 12 months.

Respondents may choose a number of solutions, and lots of did. It’s not stunning that so many organizations look like utilizing on-prem infrastructure; we’re truly shocked that the quantity isn’t increased, since in any cloud transformation, the remnants of conventional infrastructure are essentially the very last thing to vanish. And most firms aren’t that far alongside of their transformations. Transferring to the cloud could also be an necessary purpose, and cloud sources are most likely already offering crucial infrastructure. However eliminating all (and even most) conventional infrastructure is a really heavy carry.

That’s not the entire story. 29% of the respondents stated they’re utilizing a hybrid cloud (a big drop from final 12 months’s 39%), and 23% are utilizing multicloud (roughly the identical 12 months over 12 months). A multicloud technique builds methods that run throughout a number of cloud suppliers. Hybrid cloud goes even farther, incorporating personal cloud infrastructure (on-premises or hosted) working cloud APIs. When achieved accurately, multiclouds and hybrid clouds can present continuity within the face of supplier outages, the flexibility to make use of “one of the best instrument for the job” on completely different software workloads (for instance, leveraging Google Cloud’s AI services), and simpler regulatory compliance (as a result of delicate workloads can keep on personal methods).

Due to this fact, respondents who chosen “hybrid cloud” also needs to have chosen “public cloud” and “personal cloud” (or, presumably, “conventional infrastructure”). Certainly, that’s what we noticed. Solely 11% of the respondents who chosen “hybrid cloud” didn’t choose another varieties—and we’d guess that’s as a result of they assumed that “hybrid” implied the others. 27% of those that chosen “hybrid” chosen all 5 varieties, and the rest chosen some mixture of the 5 choices. The identical was true for respondents who chosen “multicloud”: solely 4% chosen “multicloud” by itself. (“Multicloud” and “hybrid cloud” had been incessantly chosen collectively.)

We’re puzzled by the distinction between 2020 and 2021. An improve in using public clouds, personal clouds, and even conventional infrastructure is smart: customers have clearly turn out to be extra snug mixing and matching infrastructure to swimsuit their wants. We don’t count on using conventional infrastructure to disappear. However why did utilization of hybrid clouds drop? We don’t have a very good reply, besides to notice that many respondents (certainly, a 3rd of the full) who didn’t choose both “multicloud” or “hybrid cloud” nonetheless chosen a number of infrastructure varieties. A mix of public cloud and conventional infrastructure was commonest, adopted by public cloud, personal cloud, and conventional infrastructure. These mixtures point out that many respondents are clearly utilizing some type of multicloud or hybrid cloud, even when they aren’t together with that of their responses.

We will’t ignore the slip within the proportion of respondents answering “hybrid cloud.” Which will point out some skepticism about this most formidable cloud structure. It may even be an artifact of the pandemic. We’ve already stated that the pandemic gave many firms a very good cause to maneuver on-premises infrastructure to the cloud. However whereas the pandemic might have been a very good time to start out cloud transformations, it was arguably a poor time to start out very formidable tasks. Can we think about CTOs saying, “Sure, we’re shifting to the cloud, however we’re maintaining it so simple as attainable” Positively.

We additionally checked out what sorts of cloud applied sciences had been engaging to completely different industries. Public clouds are most closely utilized in retail & ecommerce (79%), media & leisure (73%), and software program (72%). Hybrid clouds are strongest in consulting & skilled companies (38%), presumably as a result of consultants usually play a task in integrating completely different cloud suppliers right into a seamless complete.Personal clouds are strongest in telecommunications (64%), which was the one sector through which personal clouds led public clouds (60%).

Historically managed on-premises infrastructure is most generally utilized in authorities (72%). Different industries the place the variety of respondents utilizing conventional infrastructure equaled or exceeded the quantity reporting any type of cloud infrastructure included increased schooling (61%), healthcare (61%), telecommunications (67%), computer systems (65%), and electronics & {hardware} (58%).

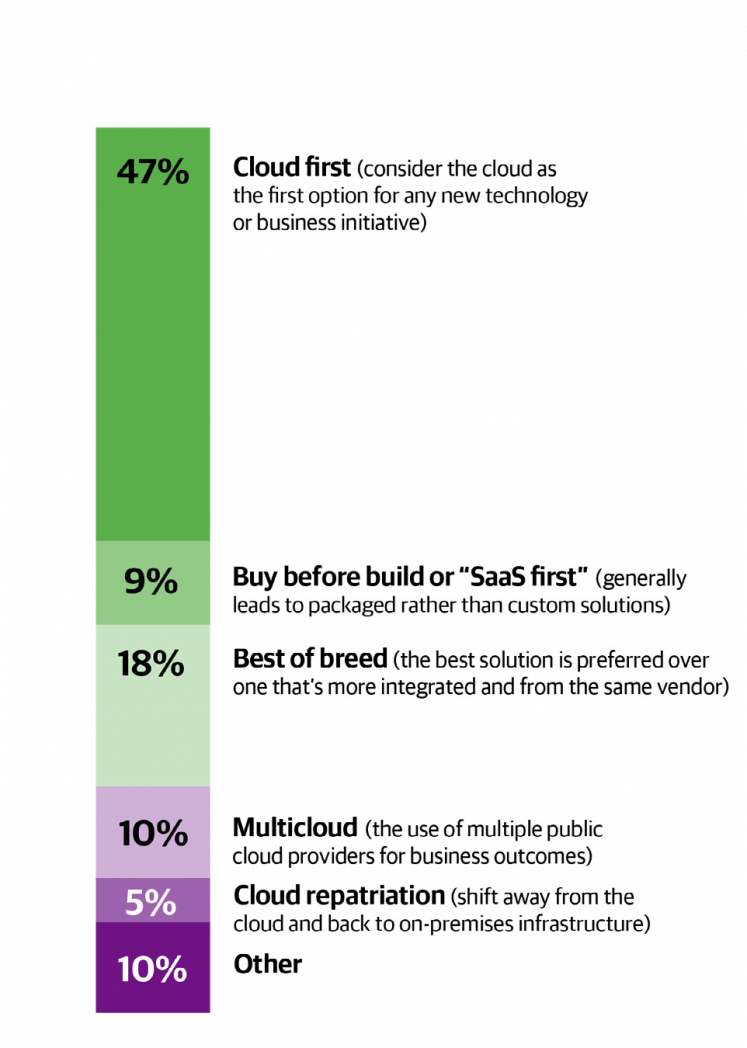

When requested about their group’s cloud technique, virtually half of the respondents (47%) answered “cloud first,” which means that wherever attainable, new initiatives take into account the cloud as the primary choice. Solely 5% chosen “cloud repatriation,” or bringing companies that had been beforehand moved to the cloud again in-house. 10% indicated a multicloud technique, the place they work with a number of public cloud suppliers; and 9% indicated that their technique is to use software-as-a-service cloud suppliers the place attainable (e.g., particular functions from firms like Salesforce and SAP), thus minimizing the necessity to develop their very own in-house cloud experience. Since “Purchase earlier than construct; solely construct software program associated to your core competence” is a crucial precept in any digital transformation, we anticipated to see a higher funding in software-as-a-service merchandise. Maybe this quantity actually signifies that virtually any firm might want to construct software program round its core worth proposition.

Our respondents method cloud migration aggressively. Virtually half (48%) stated they plan emigrate 50% or extra of their functions to the cloud within the coming 12 months; the biggest group (20%) stated they plan emigrate 100% of their functions. (We surprise if, for a lot of of those respondents, a migration was already in progress.) 16% stated they plan emigrate 25% of their functions. 36% answered “not relevant,” which can imply that they aren’t utilizing the cloud (although this is able to point out a lot decrease cloud utilization than different questions do) or that the respondent’s group has already moved its functions to the cloud. It’s most likely a mixture of each.

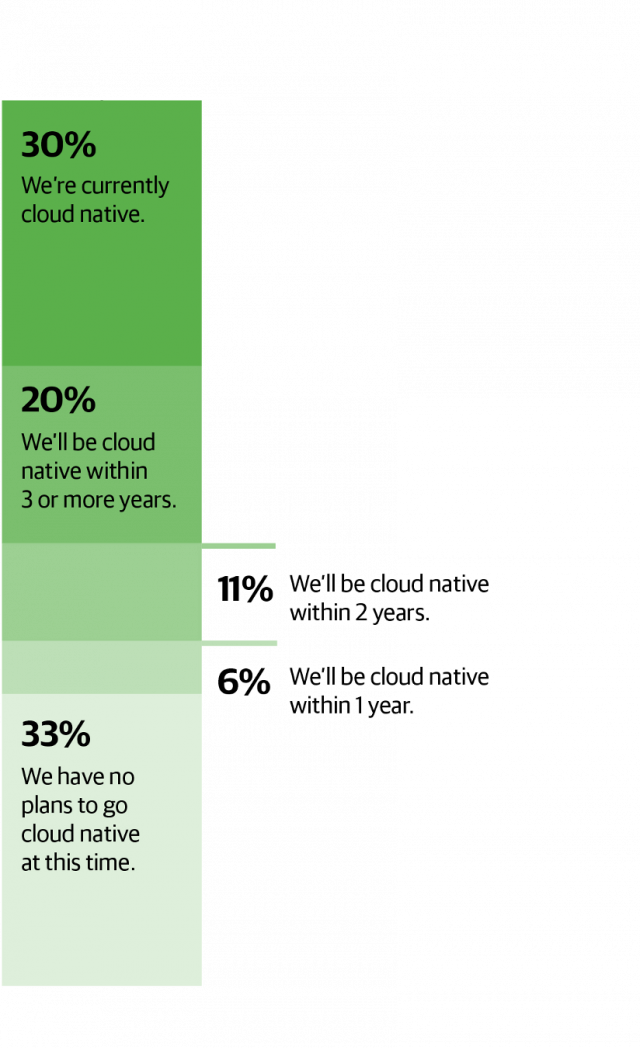

When requested particularly about cloud native improvement (constructing software program to run in a scalable cloud setting, whether or not that cloud is public, personal, or hybrid), there was an excellent cut up between those that don’t have any plan to go cloud native, respondents representing companies which are already 100% cloud native, and respondents who thought they’d be cloud native sooner or later sooner or later. Every group was (very) roughly a 3rd of the full. Trying in additional element at respondents who’re within the strategy of going cloud native, solely 6% count on to be cloud native inside a 12 months. The biggest group (20%) stated they’d be cloud native inside three or extra years, indicating a common course, if not a selected purpose.

Does the 67% who’re planning to be or are already cloud native battle with the 47% who stated that they’re pursuing a cloud first technique? It’s jarring—“cloud native” is, if something, a stronger assertion than “cloud first.” Presumably anybody who works for a corporation that’s already cloud native can also be pursuing a cloud first technique. Among the hole disappears if we embrace respondents executing a multicloud technique within the “cloud first” group, which brings the “cloud first” whole to 57%. In any case, “cloud native” as outlined by Wikipedia explicitly consists of hybrid clouds.

Maybe extra to the purpose: there’s lots of latitude in how respondents may interpret slogans and buzzwords like “cloud native” and “cloud first.” Somebody who says that their group will probably be “cloud native” sooner or later sooner or later (whether or not it takes one 12 months, two years, or three or extra years) isn’t saying that there aren’t important noncloud tasks in progress, and three or extra years hardly units an formidable purpose. However no matter how respondents might have understood these phrases, it’s clear {that a} substantial majority are shifting in a course that locations all of their workloads within the cloud.

Price and different points

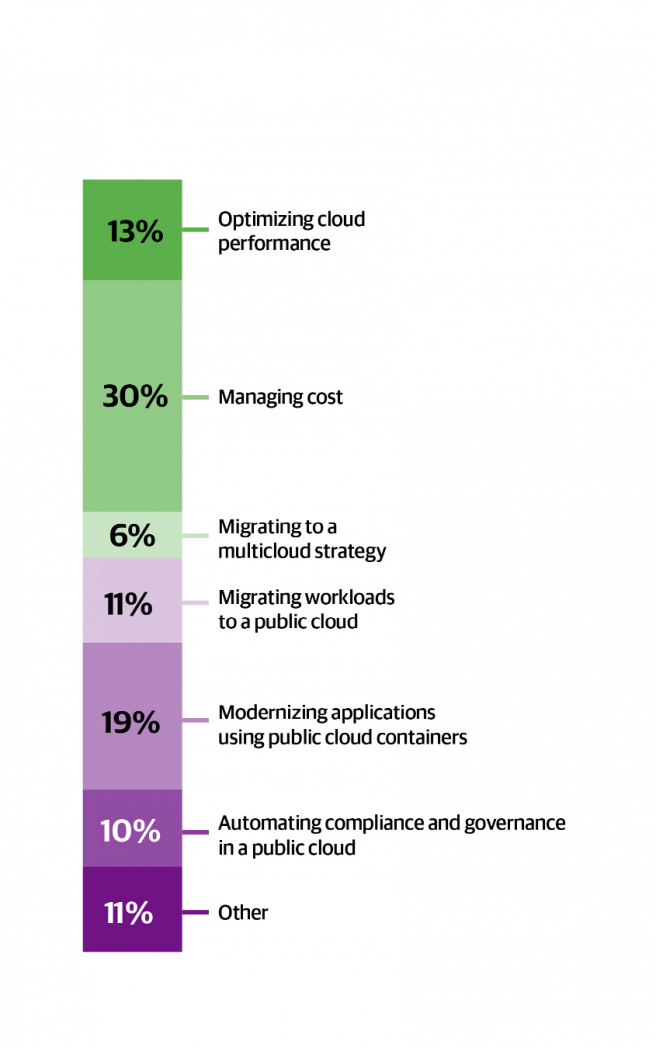

Survey respondents persistently reported that price is a priority. When requested about crucial initiatives of their organizations pertaining to public cloud adoption, 30% of all respondents stated “managing price.” Different necessary cloud tasks embrace efficiency optimization (13%), modernizing functions (19%), automating compliance and governance (10%), and cloud migration itself (11%). Solely 6% listed migrating to a multicloud technique as a difficulty—stunning given the massive quantity who stated they’re pursuing hybrid cloud or multicloud methods.

These outcomes had been comparable throughout all industries. In virtually each sector, managing price was perceived as crucial cloud initiative. Authorities and finance & banking had been outliers; in these sectors, modernizing functions was a higher concern than price administration. (23% of the respondents within the authorities sector listed modernization as crucial initiative, as did 21% of the respondents from finance & banking.)

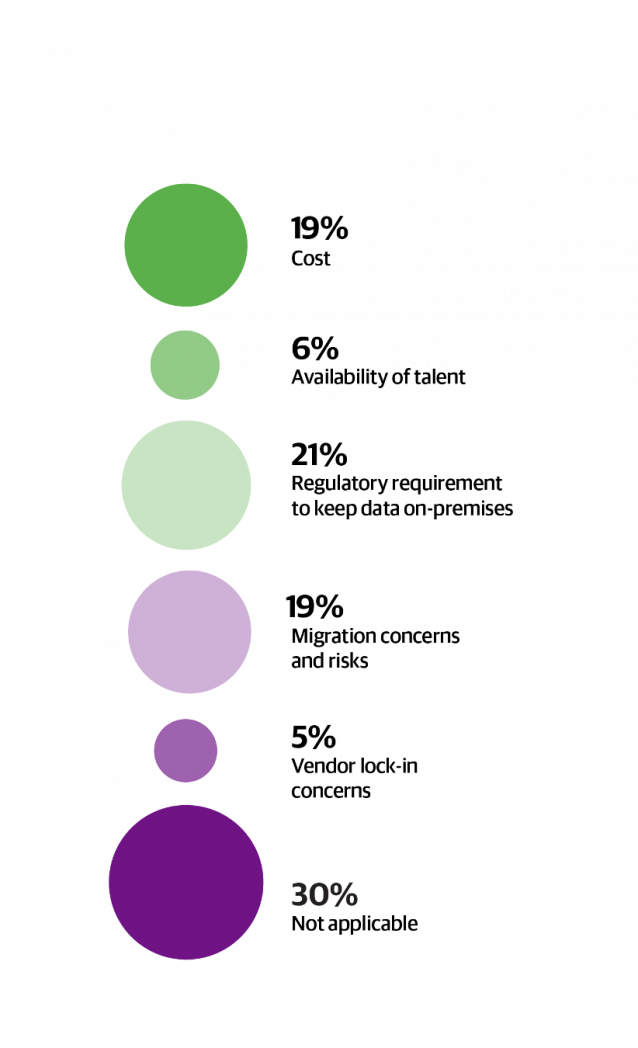

Amongst respondents who aren’t utilizing cloud computing, 21% stated that regulatory necessities require them to maintain information on-premises; 19% stated that price is crucial issue; and 19% had been involved with the danger of migration. Comparatively few had been involved concerning the availability of expertise (6%, in sharp distinction to our 2021 Information/AI Wage Survey outcomes), and 5% stated vendor lock-in is a priority. Once more, this aligns properly with our outcomes from 2020: maintaining information on-premises was the commonest cause for

not utilizing cloud computing, and value was the second, adopted by migration threat.

Why is price such a crucial issue? It’s simple to get into cloud computing on a small scale: constructing some experimental apps within the cloud as a result of you may lease time utilizing an organization bank card somewhat than going by way of IT for extra sources. If profitable, these functions turn out to be actual software program investments that you might want to help. They begin to require extra sources, and because the scale grows, you discover that your cloud supplier is getting the “economies of scale,” not you. Cloud suppliers definitely know the right way to set pricing in order that it’s simple to maneuver in however troublesome to maneuver out.

So, sure, price must be managed. And one technique to handle cloud price is to remain away. You’re not locked right into a vendor when you don’t have a vendor. However that’s a simplistic reply. Good price administration must account for the true advantages of shifting to the cloud, which normally don’t contain price. By analogy, meeting traces didn’t reduce the price of constructing a manufacturing unit; they made factories simpler. The cloud’s means to scale shortly to deal with sudden modifications in workload is value quite a bit. Do your functions instantly turn out to be sluggish if there’s a sudden spike in load, and does that trigger you to lose gross sales? In 2021, “Please be affected person; our methods are experiencing heavy load” tells prospects to go elsewhere. Improved uptime can also be value quite a bit; cloud suppliers have a number of information facilities and backup energy that almost all companies can’t afford. (At O’Reilly, we realized this firsthand through the California fires of 2019, which disabled our on-premises infrastructure. We’re now 100% within the cloud, and we’re certain different firms realized the identical lesson.)

Regulatory necessities are an enormous concern for respondents who aren’t utilizing cloud computing (21%). Once we take a look at respondents as a complete, although, we see one thing completely different. In most industries, roughly 10% of the respondents listed regulatory compliance as crucial initiative. Essentially the most notable outliers had been finance & banking (15%), authorities (19%), and healthcare (19%)—however compliance nonetheless wasn’t the most important concern for these industries. Respondents from the upper schooling sector reported little concern about compliance (4.8%). Different industries that had been comparatively unconcerned about compliance included electronics & {hardware} and media & leisure (each 3.8%). Though we’re shocked by the responses from increased schooling, on the entire, these observations make sense: compliance is an enormous situation for industries which are closely regulated and fewer of a difficulty for industries that aren’t. Nonetheless, it’s additionally necessary to look at that concern about compliance isn’t stopping closely regulated industries from shifting to the cloud. Once more, regulatory compliance is a priority—however that concern is trumped by the necessity to present new sorts of functions.

Expertise

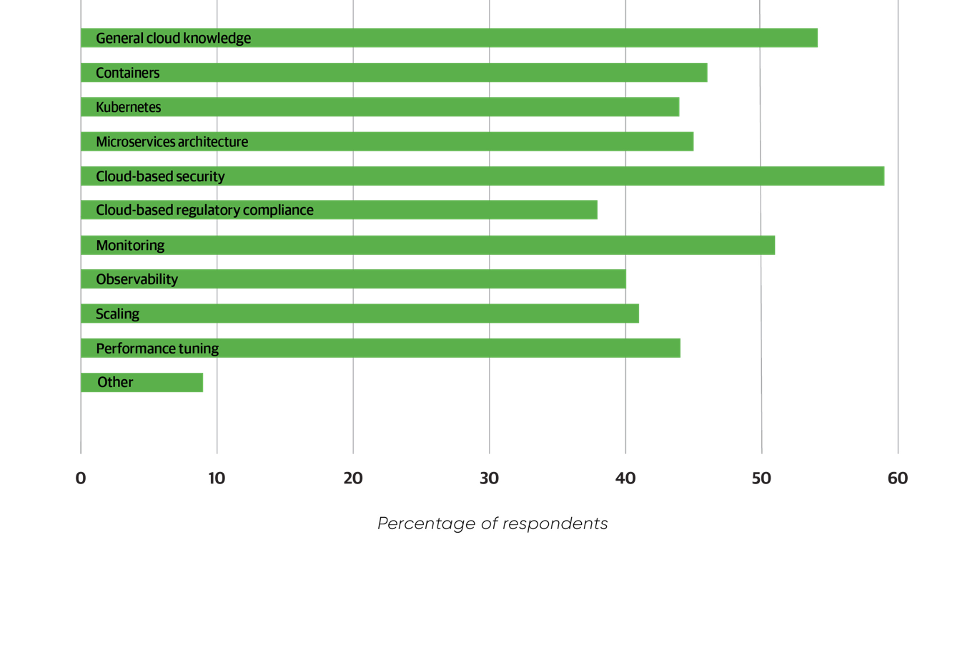

Though solely 6% of the respondents who aren’t utilizing cloud computing stated that talent availability was a difficulty, we’re skeptical about that—when you’re not shifting to the cloud, you don’t want cloud expertise. We acquired a unique reply after we requested all respondents what expertise had been wanted to develop their cloud infrastructure. (For this query, respondents had been allowed to decide on a number of choices.) The commonest response was “cloud-based safety” (59%; over half of the respondents), with “common cloud information” second (54%). That’s a very good signal. Organizations are lastly waking as much as the truth that safety is important, not one thing that’s added on if there’s time.

Maybe the most important factor to study from this query, although, is that over 35% of the respondents chosen all the expertise (besides different”). Most of them had been round 45%. Containers (46%), Kubernetes (44%), microservices (45%), compliance (38%), monitoring (51%), observability (40%), scaling (41%), and efficiency (44%) are all on this territory. Our respondents look like saying that they want every thing. All the talents. There’s undoubtedly a scarcity in cloud experience. In our lately revealed 2021 Information/AI Wage Survey report, we famous that cloud certifications had been most related to wage will increase. That claims quite a bit: there’s demand, and employers are keen to pay for expertise.

Portability between clouds

Our last query appeared ahead to the subsequent era of cloud computing. We requested concerning the obstacles to shifting workloads freely between cloud deployment platforms: what it takes to transfer functions seamlessly from one cloud to a different, to a non-public cloud, and even to conventional infrastructure. That’s actually the purpose of a hybrid cloud.

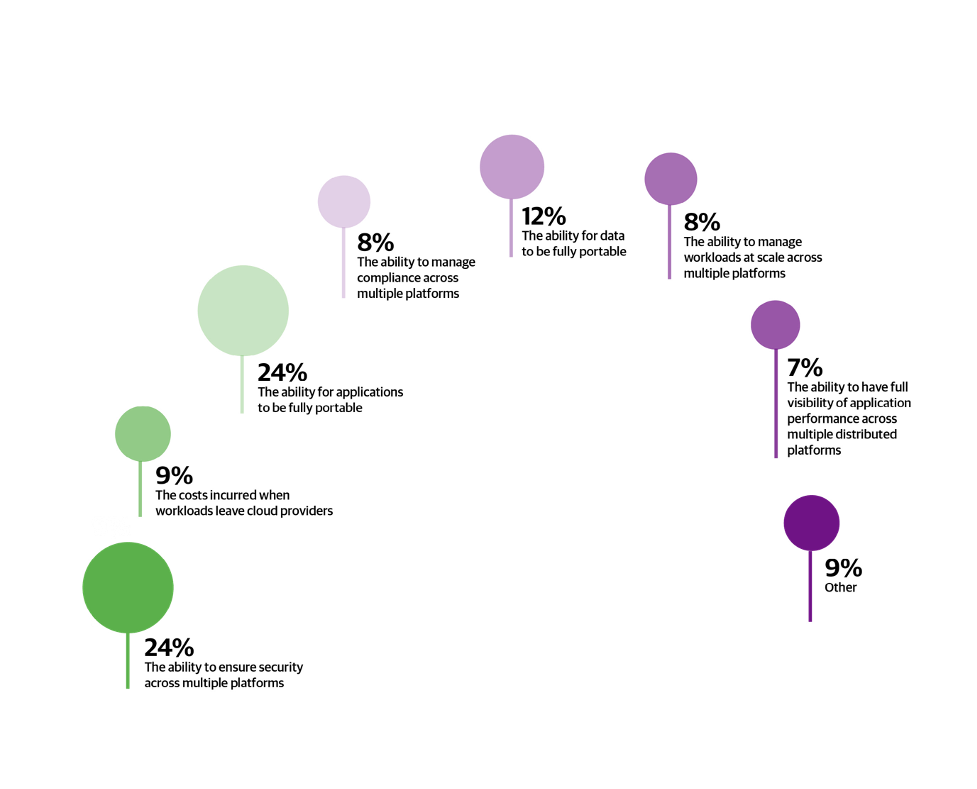

Software portability and safety had been the most important considerations (each 24%). The necessity for portability is apparent. However what might lie behind concern over portability is the string of improvement platforms which have promised software portability, going again not less than to Digital Tools’s CORBA in 1991 (and presumably a lot earlier). Containers and container orchestration are themselves “write as soon as, run wherever” applied sciences. Internet Meeting (Wasm) is the present fashionable try to seek out this holy grail; we’ll discover out within the coming years whether or not it suffices.

Safety on one platform is tough sufficient, and writing software program that’s safe throughout a number of execution environments is far more troublesome. With the rising variety of high-profile assaults in opposition to giant companies, executives have a proper to be involved. On the identical time, each safety knowledgeable we’ve talked to has emphasised that crucial factor any group can do is to concentrate to the fundamentals: authentication, authorization, software program replace, backups, and different facets of safety hygiene. Within the cloud, the instruments and methods used to implement these fundamentals are completely different and arguably extra advanced, however the fundamentals stay the identical.

Different considerations all clustered round 10%: essentially the most important embrace information portability (12%), necessary and sometimes ignored; the price of shifting information out of 1 cloud supplier into one other (9%), a priority we noticed elsewhere on this examine; managing compliance and, extra typically, managing workloads at scale throughout a number of platforms (each 8%); and visibility into software efficiency (7%).

Till subsequent 12 months

What did we study? Cloud adoption continues, and it doesn’t seem to have been affected by the pandemic. Roughly 90% of our respondents work for organizations which are shifting functions to the cloud. This proportion is simply barely bigger than final 12 months (88%) and will not even be important. (However remember the fact that whenever you’re at 90%, any additional beneficial properties include nice problem. In apply, 90% is about as near “everyone” as you will get.)

We additionally consider that we’re solely on the starting of cloud adoption. Our viewers is technically subtle, they usually’re extra more likely to be cloud adopters. A big majority of the respondents are within the strategy of shifting functions to the cloud, indicating that “cloud” is a piece in progress. It’s clearly a scenario through which the extra you do, the extra you see that may be achieved. The extra workloads you progress to the cloud, the extra you understand that different workloads can transfer. Extra necessary, the extra snug you’re with the cloud, the extra modern you might be in pushing your digital transformation even additional.

Considerations about compliance stay important. Not surprisingly, these considerations are increased amongst respondents who aren’t utilizing the cloud than amongst those that are. That’s pure—however wanting on the speedy tempo of cloud adoption in closely regulated industries like finance & banking makes us assume that “compliance” is extra of an excuse for noncloud customers than an actual concern. Sure, compliance is a matter, however it’s a difficulty that many organizations are fixing.

Managing prices is clearly an necessary concern, and in contrast to compliance, it’s a concern ranked extra extremely by cloud customers than nonusers. That’s each regular and wholesome. The frequent notion that cloud computing is cheap isn’t actuality. Having the ability to allocate a number of servers or high-powered compute engines with a bank card is definitely a reasonable technique to begin a venture, however these financial savings evaporate at enterprise scale. The cloud supplier will reap the economies of scale. For a person, the cloud’s actual benefits aren’t in price financial savings however in flexibility, reliability, and scaling.

Lastly, cloud expertise are in demand throughout the board. Common expertise, particular experience in areas like safety, microservices, containers, and orchestration—all are wanted. Whether or not or not there’s a scarcity of cloud experience within the job market, this is a wonderful time to pursue coaching alternatives. Many organizations are coping with the query of whether or not to rent or prepare their employees for brand new capabilities. When pursuing a cloud transformation, it makes eminent sense to depend on builders who already perceive your corporation and your functions. Hiring new expertise is all the time necessary, however giving your present employees new expertise could also be extra productive in the long term. If your corporation goes to be a cloud enterprise, then your software program builders must turn out to be cloud builders.

Footnote

- A short notice about precision. We’ve rounded percentages to the closest 1%, besides in some instances the place the share is small (below 10%). With practically 3,000 respondents, 0.1% solely represents 3 customers, and we’d argue that drawing conclusions primarily based on a distinction of a proportion level or two is misusing the information.

[ad_2]